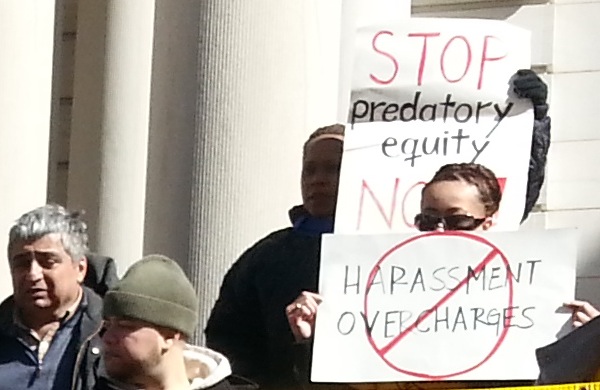

Photo by: Jarrett Murphy

At a rally at City Hall on Tuesday, advocates and tenants called on both the loan servicer and HPD to act to bring in responsible buyers.

The news on Tuesday was nothing new: Tenants were concerned about a chunk of relatively affordable housing put at risk by massive debt and deteriorating conditions.

The pattern—established at the height of the financial crisis and seen more than once since—goes like this: Real-estate investors see untapped potential profits in multi-unit buildings in moderate- and low-income neighborhoods, take out a massive loan to buy the buildings on the idea that they can ramp up the rent-roll by replacing poor tenants with richer ones and find out too late that the numbers don’t work. Starved for cash and saddled by mortgages, they defer maintenance, default on debt or both.

This time the worries are focused on a portfolio of 44 buildings in the Bronx, Brooklyn and Manhattan that were purchased by a quadriad of investors in 2007 for $133 million, with the mortgage then sold to other investors as a security. The owners of what is known as “the three-borough pool” defaulted in 2010 and went into foreclosure in 2012. Most (though not all) of the buildings have high numbers of housing code violations, and tenants and advocates are worried things will only get worse if the current owners get to refinance and retain the properties.

They’re calling on the loan servicer, LNR, to stop considering a re-fi and instead sell the buildings to a “preservation owner” for the nearly 1,600 apartments involved. LNR declined an opportunity to comment.

But at a press conference at City Hall on Tuesday, elected officials and advocates also asked the city’s Department of Housing Preservation and Development to step in and help.

“I would submit to all of you that these buildings are ‘too big to fail,'” said Councilman Ritchie Torres of the Bronx, alluding to the phrase used to describe banks and car companies during the recession. “Too big to fail at a time of savage inequalities.”

HPD funds affordable housing construction and preservation, and enforces the city’s housing code. But it doesn’t actually get to sign off on private real-estate transactions. “The role that HPD (and the politicians) can play is mostly that of speaking from their bully pulpit and trying to pressure any potential lenders not to deal with the current owners in their effort to refinance out of foreclosure,” says Andy Reicher, the executive director of the Urban Homesteading Assistance Board.

And the agency has leaned on lenders successfully in the past. When a set of 10 Bronx buildings known as the Milbank portfolio got into financial trouble and were about to be sold off in 2010 to an undisclosed bidder, Mayor Bloomberg, Council Speaker Christine Quinn and HPD all squeezed LNR, who was the servicer in that case as well, to hold off and find a buyer with a better track record. LNR relented, and a new buyer was found.

Milbank and other episodes led HPD to come up with new initiatives like the Alternative Enforcement Program and Proactive Preservation Initiative, which use fines, liens, loans and other tools to push landlords to get their buildings in shape.

Those same tools could come in handy for dealing with the three-borough pool. In addition, advocates note that most of the buildings enjoy J-51 tax exemptions, which might give the city an additional legal and financial lever to encourage a proper sale and repair of the buildings—and, says Reicher, could make what happens to this troubled portfolio “a model for what are sure to be more to come in the future.”

HPD says its code enforcement agents have been active in some of the buildings, whose conditions vary. Maintenance is the agency’s chief concern. “If an opportunity arises, we are always willing to discuss preservation options with developers who are committed to the stability of the properties and to keeping rents affordable to the current tenants,” says one HPD official.